How I Invest my Money

I’ve seen several friends lose thousands of dollars since the year started.

It wasn’t because of job loss. It wasn’t because of the pandemic.

It was because they invested everything they had into stocks like GameStop and AMC. And I saw this happen last week with Dogecoin.

By the time the general public starts investing, it’s already too late. They’re left holding the bags.

It’s easy to make fun of these people, but here’s how I see it.

- Some people were never taught anything about money.

- Society has trained us that it’s not appropriate to talk about money.

- They don’t see other paths to wealth. They’re desperate.

Social media has made it easier than ever to get caught up in hype bubbles!

If you click on one GameStop video or article, then the social media algorithms will keep sending you more of them.

You get sucked into this bubble of confirmation bias.

People have asked me over the years about how I invest my money.

I’ve always been hesitant to talk about it because of imposter syndrome. I’ve never had any formal training in investments.

I had to learn about investing the hard way. Here are some mistakes I’ve made along the way.

- I wrote in detail about how I lost money in cryptocurrency.

- I bought a ton of Apple and Amazon stock in 2009… and I sold them in 2011.

- I didn’t know how retirement vehicles worked. I invested after taxes money for years rather than invest directly into my retirement accounts.

Over the past decade, I’ve devoured countless sources of information in regards to investing, and feel comfortable enough now to talk about it.

So I’m going to share my personal portfolio and my thought process behind it.

This is the article that I wish I had to guide me years ago.

A few notes:

This is for informational purposes only and not investment advice. It’s intended to show you how I approach managing my money. Any investment comes with risks. Do your own research.

And second, you have to figure out what works best for you. I don’t know your goals. I don’t know your financial situation or how old you are. I want to plant some seeds with this article, and you can do more research on your own.

Where I Invest My Bread

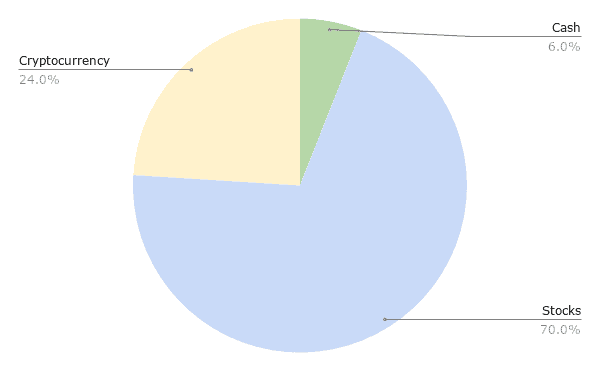

Here’s a peek at my personal portfolio.

This doesn’t include assets from my businesses.

The % changes daily because of volatility in Crypto and the Stock market.

Cash

The inflation rate is now around 2.5%. It’s possibly higher since the government keeps printing money.

This means your money in the bank is losing value.

I keep enough in the bank for my day-to-day, and we have some savings for our wedding. Experts recommend 6 to 12 months of living expenses saved up.

Hopefully, the pandemic woke everyone up to the importance of an emergency fund. An emergency fund makes your financials more robust.

I can’t think of too many emergencies that can’t be solved with credit cards.

Unless of course, someone mugs me and demands cash… ”Uhhhh… do you guys take Venmo?”

Stocks

Warren Buffett is the most successful investor in history. What does he recommend that the average person invest in?

“Invest in low-cost index funds.”

Buying an index fund share means you have a piece of ~3000 different companies. It’s an easy way to keep you diversified.

I don’t know much about the stock market. I can’t read candlestick charts or do any technical analysis.

But investing in index funds means I outperform over 90% of stock experts.

This study shows how index funds have outperformed hedge funds for the past decade.

One thing you have to watch out for is fees. They’re the silent killer… way worse than farts.

Some funds are managed by people. These suits do analysis to determine which stocks to invest in. This increases your fees.

Index funds are managed by algorithms. That’s why the fees are so much cheaper.

My Vanguard index funds have an expense ratio (fee) of 0.15%.

The average mutual fund has an expense ratio of 1%.

That 0.85% matters when it’s compounded over decades.

Do you want that 0.85% difference to go towards your future or to pay for the fund manager’s sugar baby’s monthly allowances?

Read the following article to see how important expense ratios are.

The True Cost of a 1% Expense Ratio

Next, which funds to invest in? Here’s what I do:

- 70% VTSAX (index funds for American companies)

- 30% VTIAX (index funds for international companies)

You can buy these at Vanguard.com. Why do I use Vanguard over Fidelity or their competition? Vanguard has a unique ownership structure. It’s owned by the customers. Their long-term incentives are aligned with mine.

You should figure out how to balance USA vs. international funds. I like 30% international. Most future growth is happening over in China and India. I want exposure to those markets.

I don’t own any bonds. Bonds can balance out the stocks in your portfolio. They’re much safer, but with less returns. Right now I’m young and aggressive. I want maximum growth. I’ll start allocating parts of my portfolio towards bonds once I’m in my 60’s.

Some experts recommend 110 – your age = % in stocks.

For me it’d be 110-36 = 74% stock, 24% bonds. Once again, I’m more aggressive than the average investor.

Investing in a Tax Efficiency Way

The government always wants a piece of the pie. You can invest in tax-efficient ways to legally lower your taxable income.

Here are the ways that I do it:

SEP IRA via Vanguard: 25% of my salary

(If you pay yourself $100,000 a year, then you’re able to invest $25,000 a year through a SEP IRA. There’s a catch, though. You have to extend this to every full-time employee in your company. If you’re a small operation and only work with independent contractors, then SEP IRAs are the way to go.)

Traditional IRA via Betterment: $6,000 (Max allowed)

Health Savings Accounts via Lively: $3,600 (Maxed allowed. Only if you have health insurance that qualifies)

Now that I’m about to get married, I’m slowly combining my financials with my fiancée. We’re maxing out her 401k through her work, and she has an IRA.

I actually can’t touch most of my investment funds until I’m 59.5 years old. This is a good thing. It keeps me from fucking around with my investments.

What if you want to retire earlier? There are some legal hacks.

One of the more popular ones is called a Roth IRA Conversion Ladder.

I invest a lot into my retirement. I want to make sure that I can take care of myself when I’m old. I don’t want to be a burden on my kids.

So many people don’t have retirement plans and will have to depend upon their kids. That’s the stupidest thing I’ve ever heard.

What if you’re estranged from your kids?

What if your kids won’t make enough money to support you?

The greatest thing you can do for your kids is to not be a burden to them.

You have to take care of your own future, old ass. The government is stupid—they can’t even reliably send stimulus checks to people. You don’t want to depend on them when you’re old.

Speaking of kids, how can you invest for your kid’s education? The best way is through your state’s 529. I live in Georgia, so I’m using this site.

Money Hack: You can invest for your kid’s university before they’re born. You simply open it in your name and start investing. Once they’re born, you can transfer the account over to them. Those few extra years can mean an extra 5 figures due to compounding.

The biggest thing I’m wondering about is if higher education will even be relevant two decades from now. There’s now more and more higher education alternatives such as Lambda School. Google is getting into certifications and treating them as if they’re college degrees when hiring.

Colleges are getting too expensive for the value that they’re offering. I won’t be pressuring my kids to go to college.

Cryptocurrency

I was heavy into crypto in 2017, like the rest of the affiliate industry. What a hell of a rollercoaster ride.

I invested money into Bitcoin early. Then I transferred some of those Bitcoins into altcoins. Those altcoins exploded… and then some of them crashed. Some of those altcoins I invested in turned out to be scams.

My portfolio at one point became 100% alt coins because I got greedy.

So how do I feel about crypto now?

I am bullish on cryptocurrency. I took some L’s, but I’m a better investor because of it.

Boomers were able to generate massive wealth through real estate.

Generation X were able to get into stocks during the 90s.

Cryptocurrency is our generation’s opportunity for massive wealth.

What happened in 2017 with crypto?

It reminds me of the dot-com bubble. There was too much hype and speculation before the technology and adoption were ready.

The bubble deserved to be popped.

It helps to visualize crypto like the stock market.

Coins like Bitcoin, Ethereum, Binance, Vechain, etc. are like the FAANGs. Facebook, Apple, Amazon, Netflix, and Google.

They’re the safest bets in a risky investment class.

Investing in altcoins is like angel investing. Sure, you might discover the next Uber or Airbnb. But there’s a higher chance of your coin becoming the next Enron.

There has been a lot of great progress in crypto over the past few years. Look at Decentralized Finance. There’s so much inefficiency when you cut out 5+ layers of middlemen.

Crypto is here to stay, but I don’t know which projects will be around ten years from now. That’s why I’m a lot more conservative with my investments in crypto.

If you want to keep it simple: 50% BTC, 50% ETH. Put it in a Ledger wallet. Don’t touch it for a decade.

Another way of allocating Crypto is the 50/25/25 portfolio.

50% BTC: The KING. You can’t talk about crypto without talking about Bitcoin. Network effects. Institutional investments are going straight to Bitcoin. The most battle-hardened and proven coin. This provides stability to your portfolio.

25% Ecosystem play: Ethereum, Binance Coin, Vechain, Cardano, etc. These guys are like different operating systems for blockchains. Think of it like crypto’s version of iOS vs Android. I’m personally invested in the Binance Smart Chain Ecosystem (BNB)

25% Small Cap Coins: Go to CoinMarketCap. This would be something in say #11-100. More risk, but also potentially higher returns. I’m personally invested in PanCakeSwap, and do a lot of Yield farming.

A few lessons I learned about Crypto:

- Know when to take profits. When are you going to cash out? I’ve set different formulas for myself so I don’t get caught up in emotions. For example, if / when BTC hits $75,000, I’ll cash out a percentage of my portfolio.

- Keep a certain % in Bitcoin. When there’s a bull market, the altcoins are going to rise the fastest. It’ll be tempting to move over Bitcoin -> altcoin. But sooner or later the bears will come. Bitcoin provides stability.

- Don’t get scammed. Take your coins off exchanges and into cold storage.

Real Estate: 0%

I’m not into real estate. (Although, I’m sure I have some REIT’s due to my index funds)

I like to keep my investments as simple as possible.

We’re living in Atlanta now, but we’re not sure if we’ll be staying here. So it doesn’t make sense for us to buy a home until we’re 100% sure where we want to be.

I’m not interested in being a landlord, ever.

The pandemic revealed some risks of being a landlord that I never knew were possible.

If someone doesn’t pay their rent on time, you can evict them. But then the pandemic happened. People lost jobs and couldn’t pay their rent anymore.

The CDC banned evictions. So you have landlords who are subsidizing the rent of their tenants. They’re not getting any relief from the government.

I don’t know what the answer to this problem is. But my point is that the pandemic revealed some unrealized risks in being a landlord these days.

You can always invest in REITs if you want real estate exposure, without any of the headaches.

Other Thoughts on Investing

Here are some other principles I have when it comes to investing.

Create an Automated Financial Machine with Dollar Cost Averaging

Let’s say you have $6,000 to invest this year. Most people will want to know WHEN they should invest their money.

Should they invest it all now? Will the market dip at the end of the year, and they should buy then?

I try to remove as many emotions out of investing as possible. I do dollar-cost averaging instead.

Spread that $6,000 out over the year. Automate your accounts to invest $500 every month and forget about it.

I spend less than an hour each month on my personal finances. Everything’s automated.

My bills are paid automatically. Investments are made at the first of each month.

I don’t think about money because I know my machine’s working. My emotions aren’t affected if the market’s down for the day.

Pay Off Your Debts Before Investing

I know many people are in debt. You might have student loans and a mortgage. You want to save up for a wedding, but you also want to save for retirement.

How do you balance everything?

Imagine trying to run but your foot is chained to a cannonball. That’s what it’s like to invest while you have debt.

You should figure out what your interest cut-off is. The stock market has averaged 7% returns over the past century.

4% is a solid cut-off rate.

Let say someone has the following debts:

Mortgage: 3.5%

Student Loans: 7%

Car: 8%

They should not invest at all until their car and student loans are paid off. Investing comes with risks. Paying off the car is a guaranteed 8%.

But of course, money is not just math. There’s a psychological component to it. Realize that it doesn’t have to be all or nothing. You can always put money towards the loans, and some money towards retirement.

Emotional Simplification

I designed my investments to be as simple and boring as possible. I don’t want to touch my investments outside of re-balancing it once a while.

I don’t want my portfolio to be fun or interesting. I don’t want to get dopamine fixes from my investments.

Checking my portfolio 20x+ a day isn’t productive. Bad market days can completely drain your emotions.

So that’s why I don’t invest in individual stocks like TSLA or GME. It’s why I don’t invest in altcoins anymore.

I’d get too emotionally invested.

It’s why I don’t seek alpha. Seeking alpha means to look for returns beyond the standard. I’m merely trying to “match” the standard with index funds and safe cryptocurrency.

It’s important to stay within your circle of competence.

My time and energy are better spent improving at business and marketing. That means more money I can put into the market to invest.

Once you get to a certain milestone, don’t fuck up. Meaning, I’ll reach my net worth goals soon if I stay on the path.

I won’t reach it if I start doing stupid shit and taking unnecessary risks.

Protect Your Money

Imagine if you got into a car accident tomorrow.

What happens to your money?

Can your loved ones afford a funeral for you? Or do they have to go on GoFundMe?

Can people access your bank accounts? What about your cryptocurrency?

Will the government take a huge % of your money due to estate taxes?

Will you family have to lawyer up and go through probate court?

Tony Hsieh is one of my heroes.

He did NOT leave a will for his family.

Fortunately, his father and brother were able to gain custody of his fortune.

Now people are starting to sue his estate to get a piece of the pie.

The solution is simple: create a will.

Hire a lawyer. Seriously, don’t print some shit from the internet and hope that’s enough. Hire a lawyer.

I spent several months working with a lawyer to establish my Living Trust.

This means my family avoids lawyers and probate courts. As soon as I die, everything goes immediately to them.

Put More Coals in the Fire

This is the compound interest formula.

Principal = How much money you put in.

Interest Rate = Your rate of return. For example, investing in TSLA or Bitcoin would’ve gotten you an insane return!

Time = How long you’re in the stock market.

I focus on two things.

First, I try to put as much money into my investments as possible. That’s what I mean by putting more coals in the fire.

This is as simple as increasing your income, and decreasing your salary. But sometimes simple is the hardest.

Living in the Present vs. Delaying Gratification

I was hanging out with some friends over the weekend. We were talking about how do you balance out living in the present vs. delaying gratification?

Investing is delaying gratification. That $19,000 in your 401k this year is $19,000 that you could use to live it up now.

Some people don’t believe in delaying gratification.

“I don’t know if I’m going to be alive several decades from now”

or

“I don’t want to travel the world when I’m old. This is the healthiest that I’m going to be”

There’s no correct answer to this because it’s a philosophical one.

Here’s my take on it: I try to find a balance. One framework that I’ve come up with is the minimum effective dose.

I learned about this from Tim Ferriss. Basically, what’s the least amount of effort that it takes to start getting results?

Water boils at 212F. Boiled water is already boiled. Making the water hotter will not make it “more boiled”. Instead, it’s a waste of resources. Basically, there’s a “sweet spot” before you hit a point of diminishing returns.

Let’s relate this to money.

John wants a new Tesla. Let’s say it’s $55,000 with all the bells and whistles. What is the Minimum Effective Dose? What’s the cheapest car that he’d be satisfied with?

Let’s say it’s a used Audi for $22,000. No, it’s not a Tesla and doesn’t have auto driving. But it’s still a nice and comfortable car. He scratches the itch of driving a luxury car.

But the difference is he can invest the $33,000 instead.

$33k at 7% rate of return over 20 years is $127,700. He can buy his Tesla then, and have an extra $72,000!

This is one of my approaches to decision-making.

I love staying at the Ritz Carlton and other fancy hotels. But I’ll only stay there if it’s free via credit card points. I can’t justify $500 a night for a hotel.

$150 a night in a modest hotel is good enough for me, and I rather invest that $350 a night. That’s the minimum effective dose in action. I find the “sweet spot” where I’m content, and I invest the rest. I don’t feel as if I’m sacrificing at all.

Becoming Wealthy is a Responsibility

My parents were refugees from Vietnam. They came to American with nothing.

I experienced bitterness throughout high school and college. Some of my friends got allowances and didn’t have to work in college.

I had to work at the gas station every weekend for $8.25 an hour. I was envious whenever my friends got expensive gadgets for Christmas.

And this envy put a chip on my shoulder. I channeled that energy into working 12 hours a day after college. 8 hours a day at my day job, 4 hours at night trying to run campaigns.

Eventually, I became successful.

Looking back I realized that I developed this relentless work ethic. I observed it from my parents growing up. I developed it by having to juggle so many responsibilities in college.

I view success as a duty and a responsibility.

The world has changed.

My parents didn’t have access to a 401k or know about the stock market. They just knew to buy property or to buy gold.

The world has changed. We will be going through a period of exponential growth.

So, I view it as my responsibility to understand how the modern world works.

I have a responsibility to take care of my parents when they’re older.

I have a responsibility to my future wife.

I have a responsibility to make sure my future kids learn what I was never taught. And to surpass me.

I hate when people try to virtue signal about money.

“Money doesn’t make you happy.”

“Money is not everything.”

It’s true that money alone doesn’t bring you happiness. But having money means you’re free from all the negative emotions and stress of being broke.

Where I Read About Money

Photo by David McBee from Pexels.